Debtors Control Account

What is a debtors control account?

A debtors control account is also known as a receivables control account. This is the total amount of money that is owed to the business.

Check out these links to learn more and to see another example on how to use a debtors control account:

http://www.angelfire.com/journal2/sayfol/Reading/22ControlAccounts.htmhttp://mmdk.com.pk/Receivables%20control.PDF

Also check out this video for a tutorial of debtors or receivables control accounts

Accounting - Unit 5 - Part 1 - Accounts Receivable Introduction

Uploaded by TRUTonyBell on 26 Feb 2012

Here is an example of how a debtors control

works. First we get the figures from the individual debtors’ accounts and then

move them to the control account.

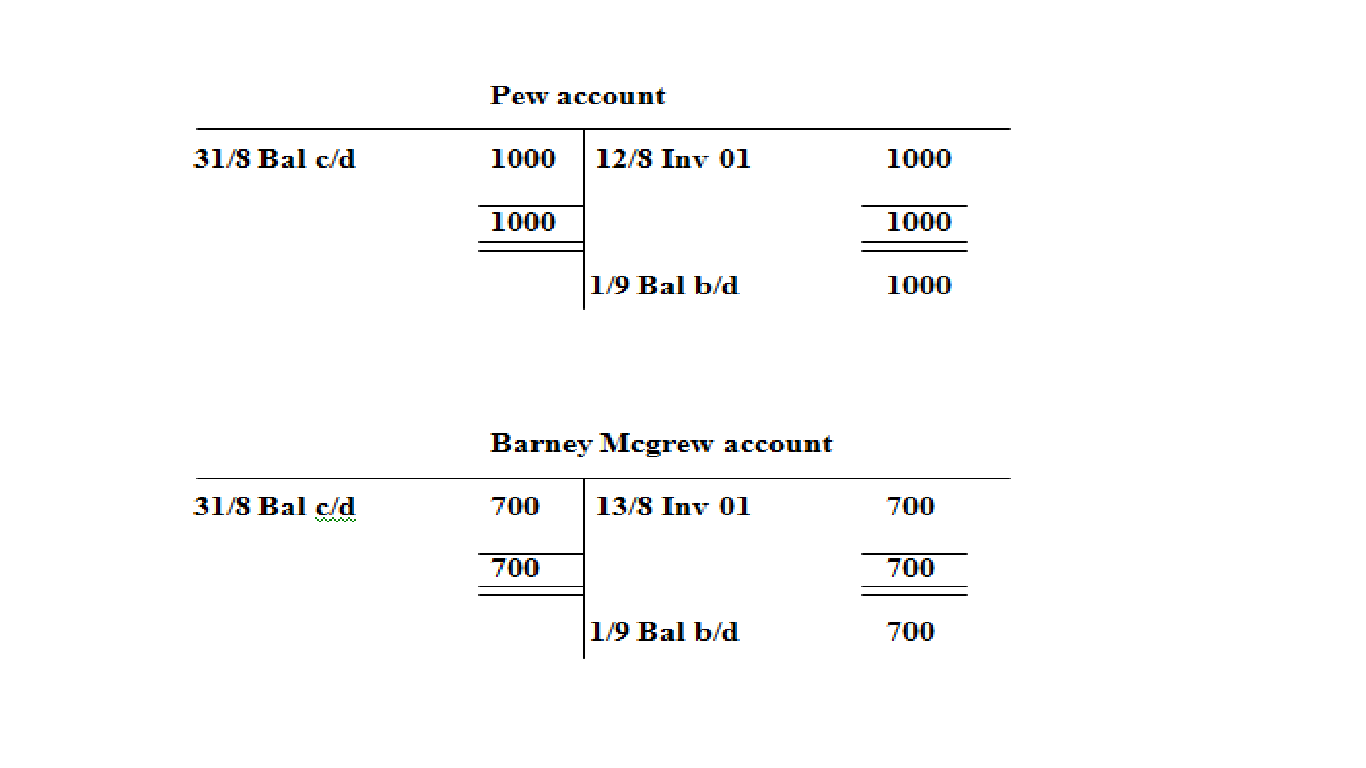

Rooney Inc. is a small company with debtors (below). This shows how the company records their debtors in their books.

The figures put into the debtors (receivables) control account are obtained from the debtors accounts.

As you see they all

balance below. The individual accounts balance with the figures in the receivables

(debtors) accounts.

Bank Reconciliation

Working together to make it balance

A bank sends out statements of customers’ accounts at certain times of the year frequently. The balance of this statement informs them of the amount that they have in their account at the date shown.

Should the bank figure be the same as the customers own books of accounts?

They should be but they hardly balance the same as you will see why.

The reason as to why they are not the same balance is due to errors or mainly due to timing differences. With timing differences this would mean that if a customer writes a cheque the bank will not notice it for maybe a week.

Even thought the customer has acknowledged this in their books, it has not being told to the bank yet.

This is also the same from the bank side. They will add items such as interest or fees that the customer will not know of until they have the bank statement.

So then whose balance is correct, the bank or the customer?

The answer simply is none of them. Adjustments will have to make in order for the figures to balance. If there are receipts, payments or both that are mentioned in the bank statement, the customer will but these into his accounts. #

Check out this video to see an example of bank reconciliation:

Here are some more videos on how to prepare a bank reconciliation statement:

Uploaded by judydaulton on 4 Oct 2010

Uploaded by judydaulton on 4 Oct 2010

Also known as a payable controls account.This is the total

amount of money that the business owes to the individual creditors. The balance

of this account must be equal to all the individual creditor accounts in the

business. These figures are obtained from the individual ledger accounts. This

is also known as the payables control account.

Here is another example of a creditors control account. Here is Ronney Inc. individual creditors accounts and its Payables (creditors) control account.

Check out this video to get more insight in producing a simple creditors control account:

Uploaded by acethejunior on 16 Jan 2012

Cash and Receivables-2 Bank Reconciliation

Uploaded by SusanCrosson on Sep 19, 2007

Here are some more videos on how to prepare a bank reconciliation statement:

Accounting - Bank Reconciliation Part I

Uploaded by judydaulton on 4 Oct 2010

Accounting - Bank Reconciliation Part II

Uploaded by judydaulton on 4 Oct 2010

Creditors Control Account

What is a Creditors Control Account?

Here is another example of a creditors control account. Here is Ronney Inc. individual creditors accounts and its Payables (creditors) control account.

As with the same with the debtors account we send the figures to the creditors control account.

The figure of 6100 is obtained from the purchases day book of the company.

Check out this video to get more insight in producing a simple creditors control account:

Creditors control account

Uploaded by acethejunior on 16 Jan 2012

No comments:

Post a Comment